Banking reform continuum

Adinkra Fram Fynn, London, UK

July 2nd, 2024

O ver the past decade, the banking sector in Ghana has gone through various stages of transformative reform. In 2017, Ghana had 36 banks. After several audits between 2017 and 2019, regulators closed nine banks. The Bank of Ghana downgraded one bank to a saving and loan, approved three mergers and oversaw one voluntary windup.

Subsequent consolidations created a new bank: Consolidated Bank of Ghana or CBG. Today, the country has 23 universal banks licensed by the central bank, the Bank of Ghana. According to the IMF article IV report (2021), Ghana’s ‟extensive banking sector clean-up, together with an improved supervisory framework, laid the foundations for financial stability”. Under the 2023 Extended Facility Agreement (ECF), the government of Ghana has announced another package of reform, which aims to further stabilize the banking sub-sector.

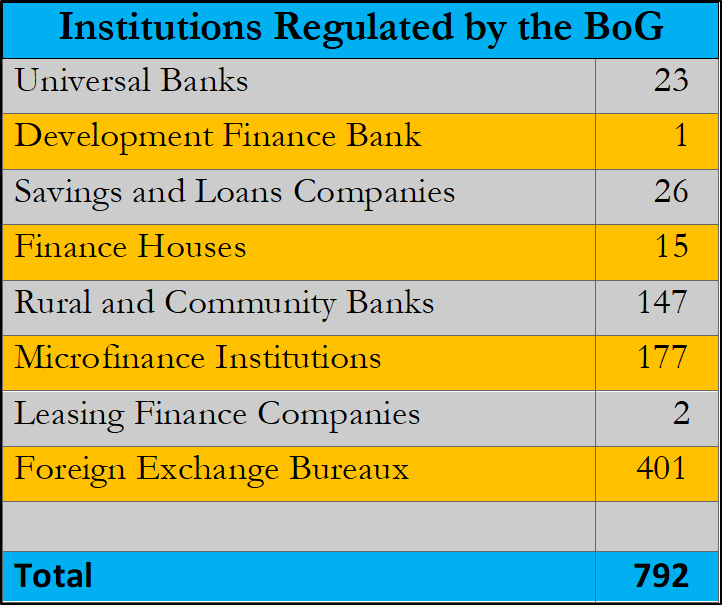

Types of Financial Institutions In Ghana

Source: Bank of Ghana, 2023

Financial sector development program

In 2020, the BoG conducted a review in the framework of the ‟Financial Sector Development Program”. This program recommened an extension of banking reforms to include specialized deposit-taking institutions (SDIs). One key aspect of this program is the increase in the capital requirement and a reduction in the leverage ratio of SDIs. During the same period, the BoG issued an ‟exposure drafts on risk and management guidelines and corporate governance and directive” for rural and community banks (RCBs).

SDIs and RCBs are important in the Ghana financial system. Their extensive network and branches across the country contribute to financial inclusion. This segment of the financial sector comprises savings and loans (S&Ls), finance houses (FHs) and mortgage institutions (MIs). They also include leasing companies (LCs) and also microfinance institutions (MFIs). Despite the economic slowdown caused by the COVID-19 pandemic, the combined assets of the SDI segment were US$1.3 billion (GH₵14.5 billion) at the end of December 2020. This represents 8.9 percent of the entire banking industry assets. Under the ECF, Ghana plans to address long-standing undercapitalization of several special deposit-taking institutions (SDIs).

Building resilience to shocks

The 2017-2019 reforms and COVID-19 policy measures showed that the banking sector is vulnerable to external shocks. Government interventions through regulatory and policy relief helped the banks to sustain these shocks. The BoG offered temporary regulatory forbearance, which included lower cash reserve requirements and lower adjusted capital requirements. At the end of 2020, solvency and liquidity improved.

According, the BoG annual report, the industry capital adequacy ratio (CAR) was 19.8 percent in December 2020. CAR therefore, was above the Bank’s minimum regulatory threshold of 11.58 percent. This implied that banks continued to have scope for lending, while maintaining capital buffers to absorb potential losses. Despite this resilience, the BoG continues to evaluate the vulnerability of the banking sector to credit tension, high interest rates, and exchange rate shocks. Through these controls, the regulator has been able to improve the monitoring of capitalization and non-performing loans (NPLs). Between 2019 and 2022, NPLs declined from 17 percent in 2019 to 15 percent.

Reforms under the ECF

The ECF requires the authorities to complete a ‟comprehensive debt restructuring; covering domestic and external debt, fiscal consolidation efforts, and other structural reforms”1. In Ghana, banks hold 33 percent of domestic public debt issued in Cedi and also in US-dollar denominated bonds. Domestic government bonds represent an important asset class in the portfolio of commercial banks, pension funds, asset management companies, and insurance companies.

By January 2024, 95 percent of domestic bond holders (including pension funds) had agreed to the exchange under the ‟Domestic Debt Exchange Program” or DDEP. The exchange covered 28 percent of outstanding domestic debt and included nonmarketable debt, arrears, and Cocobod bills2. The government offered a set of new bonds at fixed exchange proportions, with a 8.2 years and coupons of up to 10 percent.

Coupon payments represented an important stream of revenues for banks. Therefore, coupon reductions and maturity extensions caused the value of their assets to decline by 70 percent of the par value. According to the IMF, this revaluation represents a shock to the balance sheets of these financial institutions3. However, the government set up the Financial Stability Fund (GFSF) with US$250 million from the World Bank. The GFSF will provide additional liquidity against the negative impact of the DDEP. The GFSF money will disburse in phases, with an initial commitment of the U$750 million from the government of Ghana. The fund will provide a debt only (non-equity dilution) capital to foreign and local bank. On July 31st, 2023, the government announced another US$2 billion (GH₵22.8 billion) funding to further strengthen the financial system and rebuild capital buffers4.

Related Articles

BIBLIOGRAPHY

1❩ Ken Ofori-Atta (Feb 16, 2023): Statement to Parliament on “Ghana’s domestic debt exchange program”.

2❩ These are debt issued by the Cocoa Marketing Board of Ghana (COCOBOD), the commodity (cocoa trading) state-owned company

3❩ International Monetary Fund (May 2023): GHANA Request for an arrangement under the Extended Credit Facility —Press release, Staff Report, and Statement by the Executive Director for Ghana

4❩ Ministry of finance (2023): Presentation of the “Mid-Year Policy Review” to Parliament, the Minister of Finance, July 31, 2023