An abridged premier of Ghana's pension system

Aliyu Dagbani, Accra, Ghana

May 11, 2024

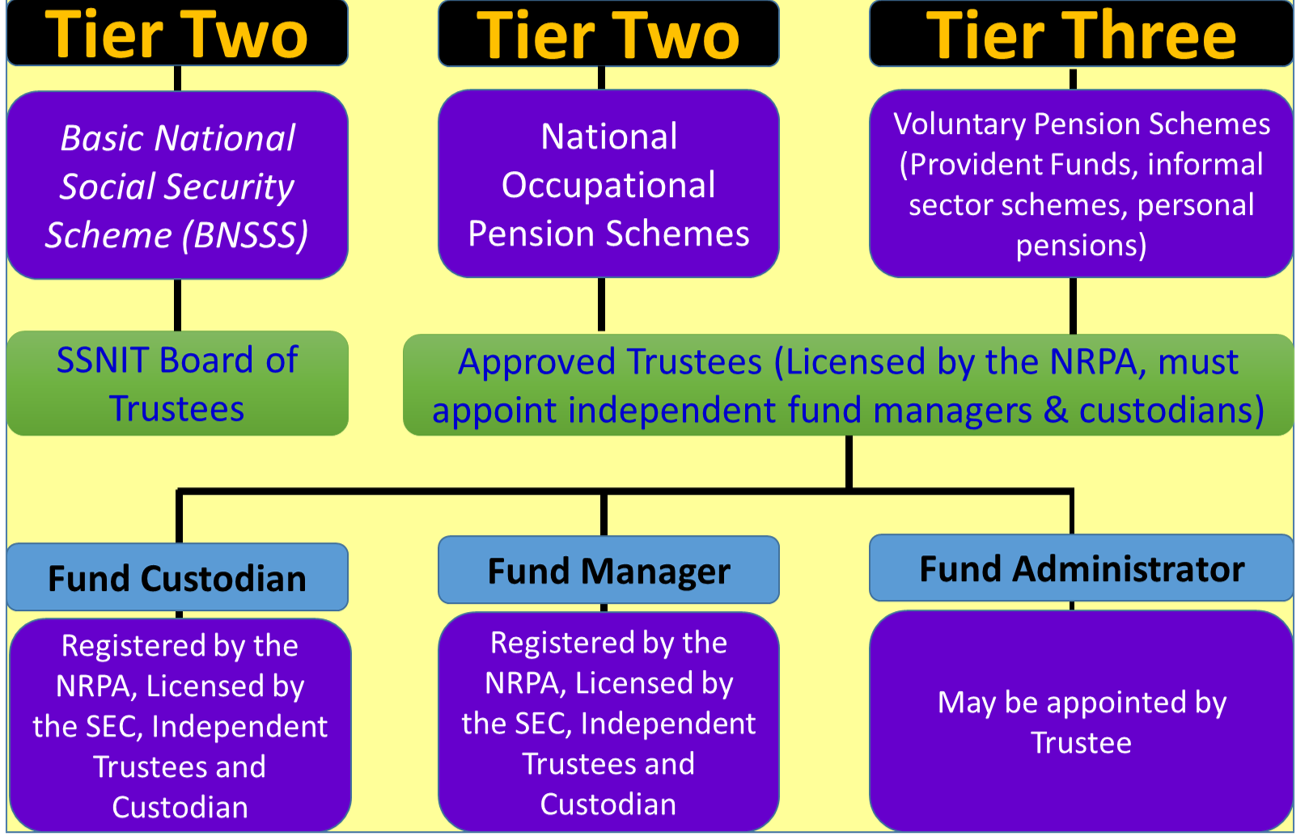

G hana launched the current pension system in 2008, after the promulgation of the National Pension Act of 2008. The act consecrated a three-tier contributory pension scheme, established the National Pensions Regulatory Authority (NPRA), and created the Social Security and National Insurance Trust (SSNIT). The pension system that emerged has two mandatory schemes (tiers one and two), and a voluntary scheme (tier three). Tiers one and two cater for the formal sector. Tier 3 is open to both formal and informal sector workers. Public, parastatal, and private institutions implement the systems under the regulatory supervision of the National Pensions Regulatory Authority (NPRA).

The pension system plays an important role in the economy through their investment in State and private securities and also in real estate. Before 2008, the State controlled the major segments of the pension system. Since the new Act, the pension system has expanded in terms of products and services and also in terms of providers. Banks, insurance companies, investment funds have become providers of pension products and services. Today the National Pensions Regulatory Authority (NPRA) supervised 39 licensed pension funds providers. In 2021, private pension funds controlled 71 percent of the industry assets. Together these companies have accumulated US$ 1.78 billion (GH₵ 28 billion) in 2021.

The pillars

Two major schemes dominate the sector. The first is the national pension scheme, established by the SSNIT under the Social Security Act of 1991 (PNDCL 247) and reviewed under the National Pensions Act of 2008 (Act 766). This is the country's sole government-sponsored pension system. Second, under the Act 766, a three-tier national pension scheme was established with effect from 1 January 2010.

Tier One

-

• The first pillar, or Tier one, is a mandatory defined benefit pension scheme managed by the Social Security and National Insurance Trust (SSNIT). The SSNIT is the main pension provider for workers in the public and private sectors. According to the 2008 Act, contributors pay a rate of 18.5 percent to the State, and remit 13.5 percent tier one. This corresponds to the approved monthly equivalent of the national daily minimum wage. Out of the 13.5 percent paid to tier one, the State transfers 2.5 percent to the National Health Insurance Fund. The SSNIT manages the manatory Basic National Social Security Scheme (BNSSS) or 1st Tier.

Tier two

-

• The second pillar of the system, Tier two, is a mandatory, but private-managed defined contribution (DC). This scheme pays lump-sum benefits financed by a contribution rate of 5 percent. In a defined contribution plan, the employer, employee or both make contributions on a regular basis. The contributions are usually invested by the fund. This means that the value of the account changes based on the contributions, investment performance, and any gains or losses. Defined contribution plans differ from traditional defined benefit plans, which guarantee a specific amount of benefits at retirement, whereas DCs do not.

-

• In this bracket, and as an illustration, the Public Sector Workers Employees' Pension Scheme (PSWEPS), established in 2018, manages tier-two pension contributions for some public sector workers. It pays a lump sum benefit to contributors when they retire, die, or are medically declared invalid. The total benefit is calculated by adding up the total paid-up monthly contributions, investment returns, and then subtracting administrative charges. A 15-member board of trustees, nominated by the government and participating institutions, manages the scheme.

Tier Three

-

• Finally, Tier three is a voluntary, private-managed, defined contribution scheme. It provides an incentive through tax exoneration to workers in the formal sector to build their own pension. In tier three, an employer has the option to set up a Provident Fund Scheme, in which the employer and employee make voluntary contributions. The fund provides tax exemption incentives for up to 16.5 percent of the employee’s basic salary. The tier three pillar also offers personal pension schemes, which target the self-employed and the informal sector. Informal workers have the option to contribute alone or as members of an identifiable group or association. They make contribution to a group personal pension scheme or as single self-employed where they pay up to 35 percent of declared income.

• Benefits from the tier three will eventually pay as an annuity. The retirement account and the savings account are not accessible before retirement and before five years. The pension system provides incentives and allows individuals and associations to take advantages of tax exonerations.

The number of active contributors on the mandatory BNSSS (first tier) was 1.7 million in 2021 and 3.2 million for the mandatory second tier. Informal sector schemes enrolled 415,950 during the same year. Formal sector employers or establishments are required to enroll under the mandatory schemes (first tier and second tier). At the end of 2021, the NRPA reported that 75,978 establishments had enrolled under the mandatory first tier. The number of establishments enrolled under the mandatory second tier also stood at 65,544 during the same year (2021 annual report of the NRPA ibid.).

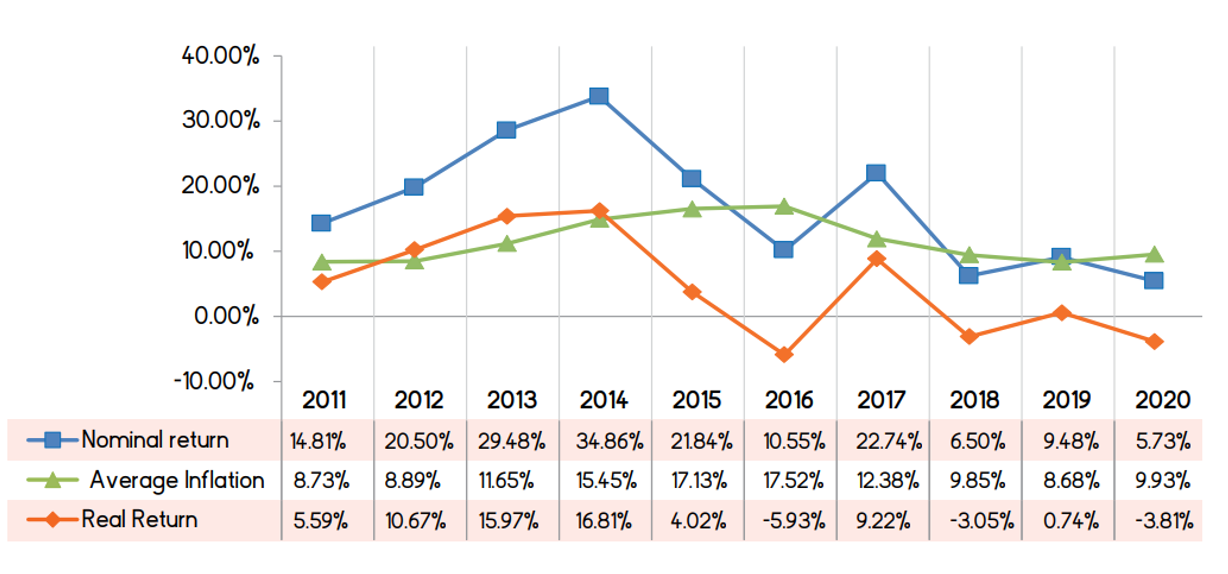

Investment Portfolio Performance from 2011 to 2020

Source: Annual Report 2020, Social Security and National Insurance Trust

Institutions

A National Pensions Regulatory Authority (NPRA) has been established to regulate all the pensions schemes. Pension funds listed on the Ghana Stock Exchange are also regulated by the Ghana Security and Exchange Commission (SEC).

The SSNIT and the NTHC

-

• The SSNIT is an agency of the government of Ghana. In April 2023, it had an active membership of over 1.8 million with over 253,617 pensioners. This institution manages 29 percent of industry's assets, making it the largest institutional investor in Ghana. The SSNIT Informal Sector Pension Scheme became operational in 2005, well before the National Pension Act of 2008. This was the first pension scheme in Ghana targeting the informal sector. Today, a subsidiary of SSNIT, the National Trust Holding Company (NTHC) manages this scheme.

Private companies

-

• Private companies which hold a license from the NPRA also offer pension products and services. The United Pension Trustees, the People’s Pension Trust, and the Daakye Pension Trust are example of established private pension institutions. Banks, insurance companies, and the Ghana Stock Exchange offer opportunities to save and invest for retirement. The emergence of FinTech has expanded the universe of pension.

Corporate pension scheme

-

• Organizations or corporations operating in Ghana can opt for a group or corporate pension scheme, in addition to the BNSSS. This is the case for the Ghana Cocoa Board (COCOBOD), which established the Cocoa Farmers Pension Scheme in 2018. The scheme is accessible to the 850,000 cocoa farmers across the country, through a group personal pension scheme, which combines tier two (mandatory) and tier three (voluntary) contributions. Farmers make voluntary contributions towards their retirement while COCOBOD makes a supplementary contribution on behalf of the farmers.

Public and private pension schemes can also offer other mechanisms to contribute to and complement the national health insurance scheme, which provides healthcare to more than half of the population of Ghana.

Reform

Pension companies hold a proportion of government bonds and also shares of listed companies. They also have substantial investments in real estate, for example commercial properties, social housing, and premium residential estates. Between 2011 and 2014, despite economic turbulences, SSNIT investments beat inflation. It has, however, underperformed since Ghana went into a debt crisis at the end of 2022.

Investment Portfolio Performance from 2011 to 2020

Source: Annual Report 2020, Social Security and National Insurance Trust

Between 2016 and 2020, for example, the SSNIT investment portfolio grew from US$717 million to US$1 billion. During this five-year period, the portfolio allocated 46.45 percent to domestic equities, 23.75 percent to the government of Ghana fixed income, and 29.80 percent to alternative investments. In recent years, because of high inflation and a turbulent economic environment, the pension fund has experienced a slight increase in liabilities compared return from its assets and also debt.

Private pension funds have also experienced a stagnation and even a decline in assets especially after the domestic debt restructuring of 2023.

According to the International Labor Organization (ILO), the government of Ghana completed the actuarial valuation of the Social Security and National Insurance Trust (SSNIT) in November 2020. The valuation was carried out after consultations with relevant stakeholders including the Ministry of Employment and Labour Relations and the social partners.

To improve the financial sustainability of the SSNIT, the ILO recommended an adjustment of pensions according to salary growth and instead adjust to inflation. It also recommended the implementation of rules in the funding policy to deal with situations where salary increases are lower than inflation. Finally, the ILO suggested a change of the financial reporting from a cash to an accrual basis as well as schedule increases of contribution rate increases according to a funding policy11.

Related Articles

BIBLIOGRAPHY

1❩ GCB Bank (2022): Sector Industry Analysis – Commodities Report (Rice & Sugar) Imports 2022, By GCB Strategy & Research

2❩ IDH (2023): Transforming Ghana’s Rice Sector: Stepping Up with Inclusive Solutions - https://www.idhsustainabletrade.com/news/transforming-ghanas-rice-sector/#:~:text=Ghana%20currently%20consumes%20about%201.5,farmers%20practice%20rain%2Dfed%20agriculture .

3❩ Ministry of Food and Agriculture (2020): Rice Strategic Brief - https://mofa.gov.gh/site/images/pdf/Strategic_Brief_Business_Model_rice.pdf

4❩ G.Kranjac-Berisavljevic’, R.M. Blench and R.Chapman (2003): Rice production and livelihoods in Ghana, Overseas Development Institute (ODI) and University for Development Studies, Tamale, Ghana

5❩ Ghana Investment Promotion Centre - GIPC (2020): Ghana’s Agriculture Sector Report

6❩ FAO (2015): FAO Supports Sustainable Increase in Rice Production and Productivity of Small and Medium Scale Farmers through a Public Private Partnership - https://www.fao.org/ghana/news/detail-events/en/c/379087/

7❩ United Nations Industrial Development Organization - UNIDO (2022): Improving the quality of post-harvest processes in Ghana’s rice value chain - https://www.unido.org/news/improving-quality-post-harvest-processes-ghanas-rice-value-chain

8❩ World Bank (2013): Smallholder Rice Farmers in Ghana’s Kpong and Weta Irrigation Projects - https://microdata.worldbank.org/index.php/catalog/5863

9❩ African Development Bank (2001): Ghana Inland Rice project - https://www.afdb.org/fileadmin/uploads/afdb/Documents/Project-and-Operations/GH-2001-050-EN-ADF-BD-WP-GHANA-AR-INLAND-VALLEYS-RICE-DEVELOPMENT-PROJECT.PDF

10❩ https://mofa.gov.gh/site/brief-on-the-european-union-ghana-agriculture-programme-eu-gap-in-savannah-ecological-zone

11❩ ILO (2020): Actuarial valuation of the Social Security and National Insurance Trust schemes as at 31 December 2020 https://www.social-protection.org/gimi/Contribution.action;jsessionid=_zFHzbOyEZMpaXAMVrIz8TuBUMnIj2URonK4PDLhF2LVWfuwMhl_!256579239?id=897