Managing relations with Eurobond holders during and after restructuring

Hudson-Odoi Deladem, New York, NY, USA

January 10, 2024

S overeign defaults are a recurrent events in modern finance. Default is often the outcome of severe domestic economic problems, internal financial or management problems, external shocks, wars, and global crisis such as health pandemic. Default is preventable, but when they happen, restructuring aims to secure the creditor’s interest and to give the debtor the opportunity to repay with flexible terms. Ghana is an interesting case because it defaulted after a decade-long period of sustained and remarkable economic performance. Thus for Ghana, a fluid restructuring will maintain working relations with bondholders and facilitates a return to the international capital market.

Ghana Eurobond issues

Ghana issued its first Eurobond in 2007. The 10-year Eurobond raised US$750 million at a coupon of 8.5 percent. At that time, analysts described the issue as a breakthrough that made Ghana the first nation in Sub-Saharan Africa, after South Africa, to tap Eurobonds. Between 2013 and 2021, Ghana issued other Eurobonds.

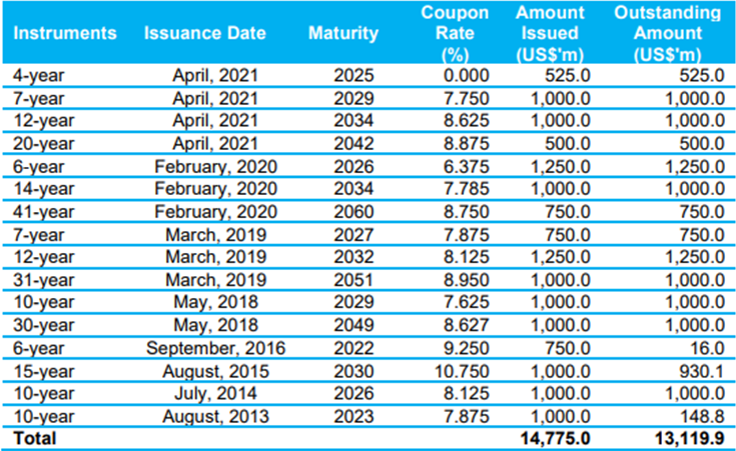

Outstanding Eurobond issuance (Q4 2021)

Source: Ministry of Finance, Ghana

In March 2021, Ghana issued her ninth Eurobond, which raised US$3.00 billion. The bond had four tranches with different duration, yield, and nominal target value. The first was a 4-year zero coupon Eurobond of US$525.0 million with a yield of 6.309 percent at maturity. Then, three additional tranches had coupons payments over 7-year (value US$1 billion), 12-year (US$1 billion), and 20-year (US$500.0 million). These last three coupons had respective rates of 7.750 percent, 8.625 percent, and 8.875 percent.

Distress

This is not the first time Ghana is resorting to debt restructuring to restore debt sustainability1. In the 1980s and 1990s, the country went through debt cancellation, debt relief initiatives and bilateral debt rescheduling. On yet other occasions, it refinanced its outstanding debt through borrowing, by using parts of the proceeds of the Eurobond issue, to repay of maturing bonds. Since independence, on 17 different occasions, successive governments have sought the intervention of the IMF during economic distress.

The restructuring of Eurobonds is complex because of their characteristics. At inception, they are attractive because of their homogeneity. Unlike sovereign bonds issued under myriad domestic laws and in local currencies, Eurobonds have in-built mechanisms, such as the collective action clause (CAC) that facilitates debt restructuring. But investors will require high yields and short-term conditions for an emerging economy like Ghana, because of poor credit ratings and perceptions of high risk. Market participants see a strong correlation between sovereign ratings and default2. The country must therefore accept high interest rates, high coupon payments, and short maturities for any additional financing in restructuring situations.

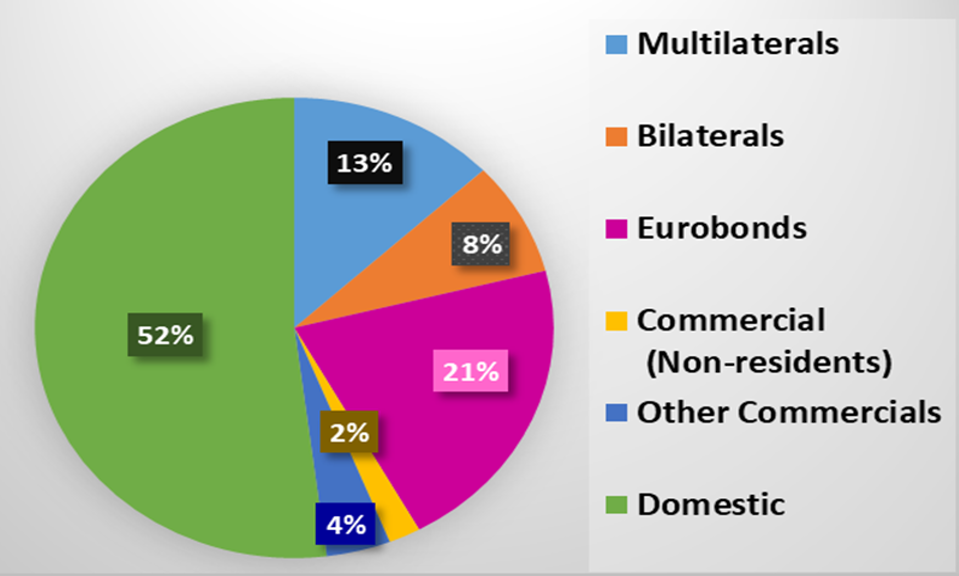

Breakdown of government debt Pre Domestic Debt Exchange

Source: International Monetary Fund, 2023

Relations with creditors

Ghana’s Eurobonds attracted a diverse pool of investors. But in a situation of distress, this diversification becomes a problem. Ghana will need to convince a large proportion of creditors, and prepare them to absorb some losses. If bondholders cannot agree, or if they are not getting acceptable terms from the restructuring, a stalemate arises. Dissatisfied investors will use their legal prerogatives in the bond covenant to secure improved terms. Such disputes lead to less debt relief and prolonged litigations3. But, when creditors collaborate to channel the requirements of individual bondholders, the restructuring process reduce the probability of individual litigations. In these circumstances, a proactive management of relations with Eurobond holders is critical during and even after the restructuring process.

Ghana’s Eurobonds formed a creditor committee (the ‟Committee”) on December 19th, 2022. The Committee includes mutual funds, asset managers, insurance firms, hedge funds, and boutique investors.

In a statement, the Committee advocated an ‟orderly” and comprehensive debt restructuring, while recognizing that such resolution will require fair burden-sharing. For the Committee, an active collaboration between the Ghanaian authorities, private creditors (both domestic and international) and official sector creditors is essential. The Committee welcomed the signing of a three year extended facility agreement between the IMF and Ghana4.

The Committee said that it wants to secure an outcome that is ‟equitable” for creditors and also responsive to the economic and social challenges facing Ghana. ‟A key factor in measuring the success of Ghana’s debt resolution will be the timely restoration of international market access, which remains critical for Ghana to meet its development objectives” the Committee said.

Related Articles

BIBLIOGRAPHY

1❩ Bank of Ghana (2015): Policy Brief - https://www.bog.gov.gh/wp-content/uploads/2019/07/THE-HIPC-INITIATIVE-AND-GHANA-policy-brief-1.pdf

2❩ S&P Ratings (2022): Transition, and Recovery: 2021 Annual Global Sovereign Default And Rating Transition Study - https://www.spglobal.com/ratings/en/research/articles/220504-default-transition-and-recovery-2021-annual-global-sovereign-default-and-rating-transition-study-12350530

3❩ Chuck Fang, Julian Schumacher, Christoph Trebesch (2020): Restructuring sovereign bonds: holdouts, haircuts and the effectiveness of CACs - Working Paper Series, European Central Bank.

4❩ International Monetary Fund – IMF (2023): Request for an arrangement under the extended credit facility – Debt sustainability analysis - https://www.elibrary.imf.org/downloadpdf/journals/002/2023/168/article-A002-en.pdf