Repurchase Agreement (Repo) in Ghana: Market, risks & prospects

Gifty Yaaba, Atlanta-GA, USA

January 05, 2024

A Repo is an agreement between parties, in which one party (buyer) agrees a temporary sale of a security (a basket, group of securities). The transaction contains a commitment by the second party (seller) to buy the security (or a basket or group of securities) back from the purchaser. This second purchase will have a specified price at a designated future date. In Ghana, bilateral contracts dominate the market. The Ghana Central Security Depository (CSD) safe-keeps the securities (or a basket or group of securities) on behalf of the parties to the transaction. The borrower (Repo) provides collateral in return for cash, while the lender (reverse repo) provides cash and receives collateral in return (e.g. treasurers or money market funds).

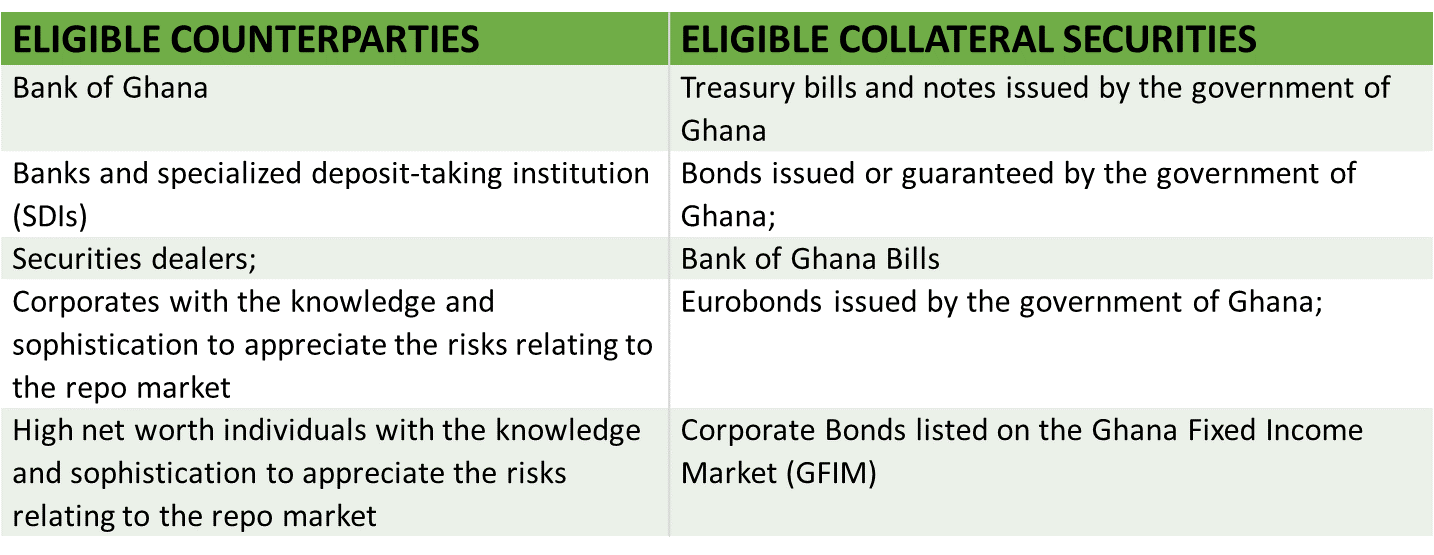

Repo guidelines in Ghana

The 2019 guidelines for repos prescribes that the minimum purchase price for repo transactions involving corporates and high net worth individuals is at least US$83,309 (GHS1,000,000). This threshold is for transactions denominated in Ghana Cedi or its equivalent in any other currency. Regulators do not prescribe a minimum requirement for banks, SDIs (specialized deposit-taking Institution) and also securities dealers.

Also, according to the guideline, the maturity of a security (collateral) must be shorter than the maturity of the repo agreement. Corporates not domiciled in Ghana shall not transact repos, where the collateral securities have time to maturity of less than two years. Securities are not eligible as collateral if they serve as guaranteed elsewhere for the seller.

Repo basic features

The features of the repo instrument vary in terms of maturity, types of collateral or whether they have specified term or are open-ended. They also vary in terms of ‟the haircut” (i.e., the difference in value between the securities sold and cash delivered) and pricing.

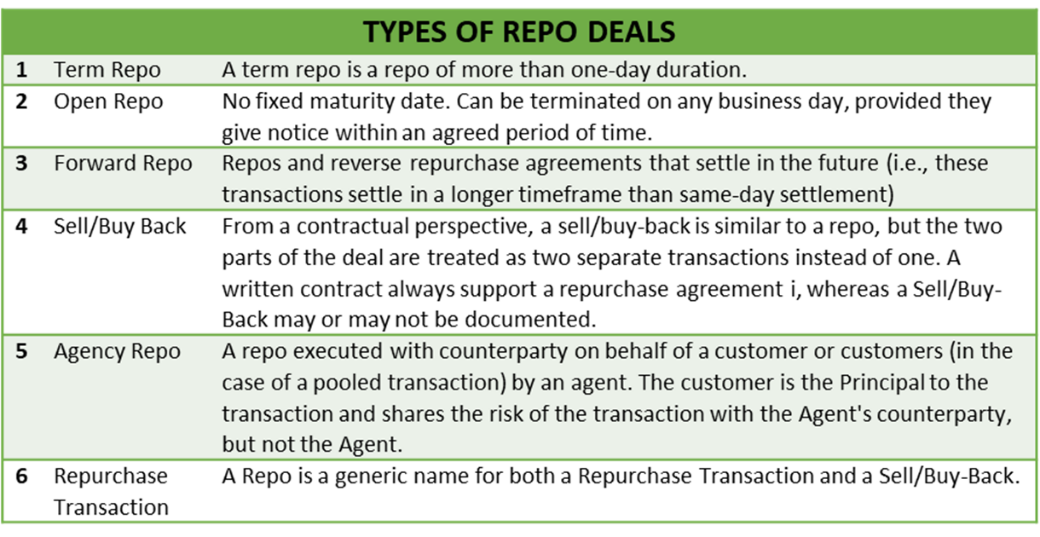

The Global Master Repurchase Agreement (GMRA) recognizes six types of contracts. The GMRA contains standard provisions suitable for the common repos transactions. Countries supplemented the GMRA with domestic laws.

Interbank liquidity

In Ghana, repo instruments have an economic function as a key money market instruments that help banks and other market participants to mobilize short-term financing. The Bank of Ghana and pensions are the largest and active participants. In 2022, 69.4 percent of classic repo transactions were transactions executed and settled among the Bank of Ghana and the commercial banks. During the same period, transactions between commercial banks represented 30.6 percent. The smallest share of transactions occurred between commercial banks and the State pension fund SSNIT (Social Security and National Insurance Trust), for a value of US$ 416,545 (GH₵5.0 million). Between 2021 and 2022, the dollar value of repo transactions increased by 31.9 percent to US$27.6 million (GH₵334.6 million) from US$21 million (GH₵253.7 million) in 20211.

Systemic risks

Empirical studies2 from other markets show that during sovereign default, repo markets have a tendency to become a potential transmission channels of systemic risk. Another source of systemic risk for repos is the concentration of ownership of domestic bonds, which serve as collateral. According to the IMF, domestic debt reached 45.7 percent of GDP in 2022. The BoG held the equivalent of 16 percent. Commercial banks own 33 percent domestic debt3. In the current context high inflation and rising interest rates, the private is essentially able to monetize government securities through repos.

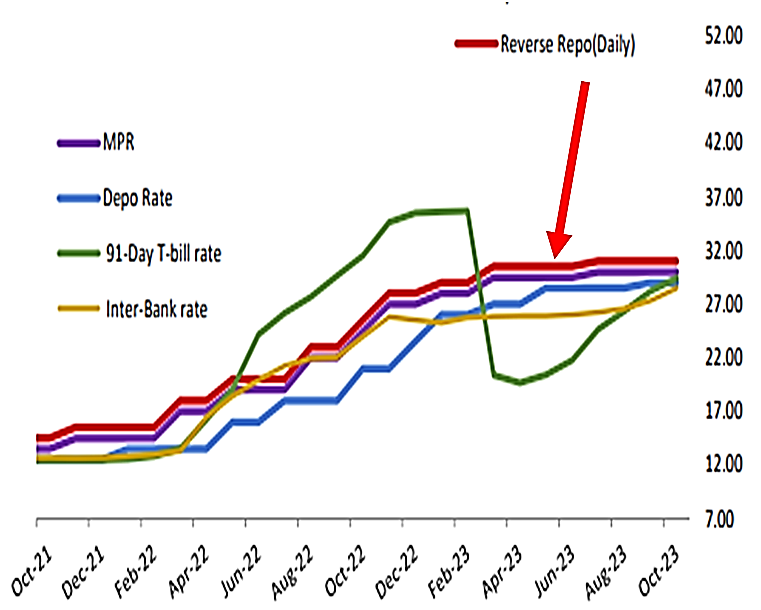

Between 2021 and 2023, interest rates, including repo rates rose, as the country tamed inflation. Throughout the fiscal year 2023, the spread between the four main benchmark rates narrowed (interbank offer rate, the monetary policy rate and Tbill rate and the repo rate). This reflected the fact that borrowers were pledging collaterals that were also carrying the consequences of the distressed economic environment. Under non-distress environment, an increase in repo rates translates into a rising cost of borrowing, while a decrease has the opposite effect (holding other parameters constant). It reduces the cost of borrowing and results in more liquidity in the economy.

Benchmarking the Repo rate

Source: Bank of Ghana November 2023

The government is addressing these systemic risks. In 2023, the country concluded a debt exchange program with domestic bond holders and an external facility agreement with the International Monetary Fund (IMF). In January 2024, authorities announced the signing of a moratorium4 with official creditors under the G20 Common Framework, for a comprehensive debt restructuring5. In June 2024, Ghana also reached an agreement in principle with bondholder groups to restructure around $13 billion of Eurobonds. The country is on a recovery path. Despite volatility and spikes, inflation is falling, the national currency is recovering on the back of a modest economic growth in 2023 and the first half of 2024. An improvement of the economic situation of the country augurs a recovery for the repo market.

Related Articles

BIBLIOGRAPHY

1❩ Ghana Central Securities Depository (CSD)

2❩ Angela Armakola et al (2020): Repurchase agreements and systemic risk in the European sovereign debt crises: the role of European clearing houses - https://hal.science/hal-01479252/document

3❩ IMF (2023): Ghana: Request for an Arrangement Under the Extended Credit Facility-Press Release; Staff Report; and Statement by the Executive Director for Ghana - https://www.elibrary.imf.org/view/journals/002/2023/168/002.2023.issue-168-en.xml

4❩ https://mofep.gov.gh/index.php/news-and-events/2024-01-12/%20%20ghana-reaches-agreement-with-official-creditors-on%20debt-treatment-under-the-g20-common-framework

5❩ Ministry of Finance (January 2024): Ghana Reaches Agreement with Official Creditors on Debt Treatment Under the G20 Common Framework - https://mofep.gov.gh/sites/default/files/news/Ghana-Reaches-Agreement.pdf