A modern monetary policy for economic transformation

Balima Dangana, Accra, Ghana

February 17, 2024

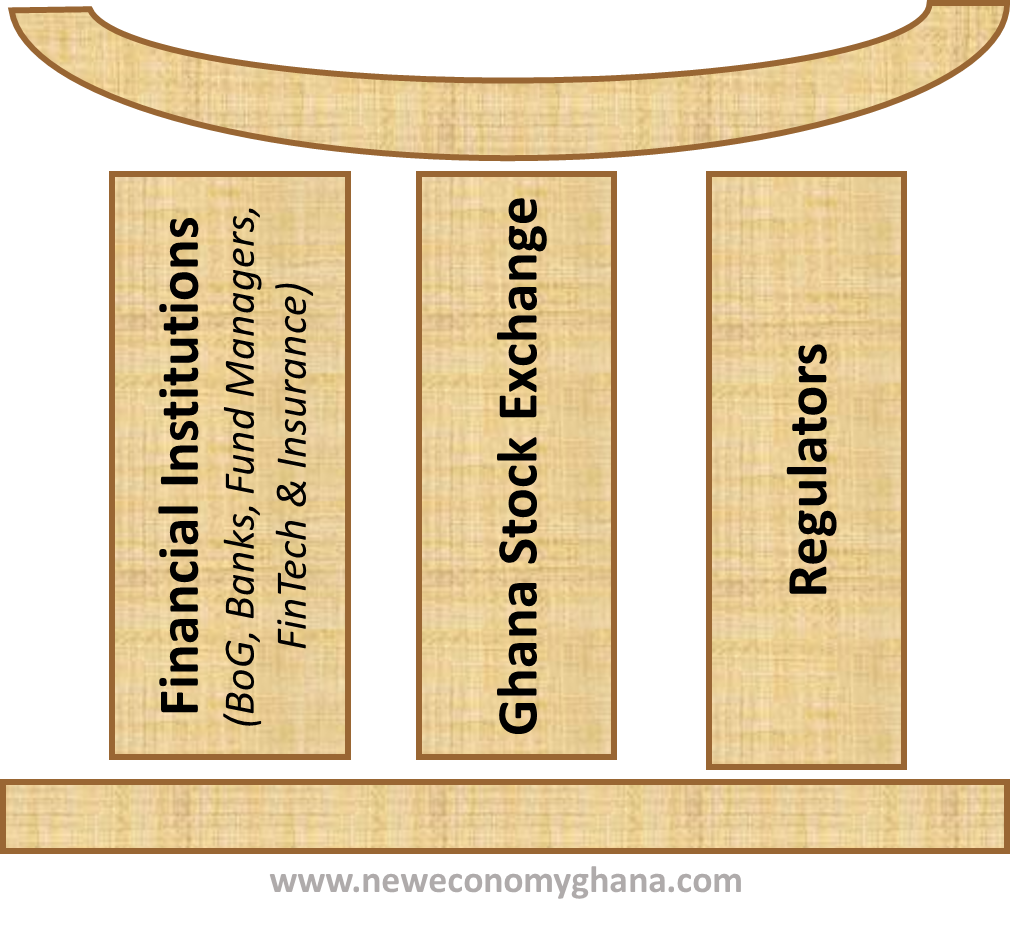

T he financial system of Ghana has pillars. The central component is the Ghana Stock Exchange. Financial institutions, including the the Bank of Ghana and commercial banks, fund managers, insurance companies, brokers form the second pillar. They offer a variety of services and products to customers. The last component groups state institutions and financial regulators.

The ministry of finance and the Bank of Ghana are quati-regulators and also issuers of securities. Examples of regulators include the Security and Exchange Commission (SEC), the Insurance Commission and the National Pensions Regulatory Authority (NPRA). In this universe, the Accounting Standard Board also has the function of a quasi-regulator of accounting standards.

As the regulator of banks, the BoG is a pivot of the entire financial system. Its mission is to ensure an efficient operation of the banking and credit system and maintain the stability of the financial system. The BoG has the mandate to monitor inflation, currency volatility, and maintain sufficient reserves. It contributes to the collective pursuit of economic growth and development.

Pillars of the Ghana Financial System

Reform

In 2002, a new law established a Monetary Policy Committee (MPC). The Governor of the Bank of Ghana chairs the MPC. This body meets every two months to assess current economic conditions and the inflation outlook. In 2007, the BoG adopted an inflation targeting (IT) framework and a flexible exchange rate regime. Today the BoG relies on this framework to ensure price stability over the medium-term. The Bank’s inflation target is 8 percent.

The emergence of crypto-assets and FinTech prompted the bank to develop a regulator sandbox to promote innovations. This includes blockchain based e-KYC (electronic know your customer) platforms, RegTech (regulatory technology) and on SupTech ( supervisory technology). The sandbox also contains plans for digital banking, financial inclusion, and payment solutions for micro, small, and medium-size enterprises1.

Responding to economic turbulence

On December 19th, 2022, Ghana signed an Extended Credit Facility (ECF) with the IMF following the country's default on debt2. The ECF prescribes a package of economic reforms. As part of the reform, the BoG is developing plans to abandon the monetary financing of the economy. The Bank will also unify and reinforce flexible exchange rate.

A Memorandum of Understanding (MoU) signed in May 2023 between the ministry of finance and the BoG contains guidelines on this new fiscal discipline. The government and the central bank want to maintain a tight ‟restriction of central bank financing” at least during the three years of the ECF program3. Specifically, authorities plan to revise the Bank of Ghana Act 2002 (Act 612), to lower the overdraft limits, enhance compliance, and limit breaches.

In the framework of the ECF, the BoG and the IMF agree that monetary and exchange rate policies need to focus on reining in inflation and on rebuilding foreign reserve buffers. Gross International Reserves (GIR) was US$6.87 billion at the end of Q3 of 2024, equivalent to 3.1 months of import cover. The GIR has grown, but, still has not reach the position achieved at the end of December 2021 when it reached US$9,695.2 million (which was equivalent to 4.3 months imports cover)4.

From the beginning of the year to 19th July 2024, the Ghana Cedi depreciated by 19.6 percent against the US Dollar, compared with 22.1 percent for the same period in 2023. The Bank of Ghana responded with a combination of monetary policies instruments. It continues to tightened monetary policy stance and has implemented a dynamic Cash Reserve Ratio (CRR) to mop excess liquidity. The Bank has revised regulations on advanced payments for imports by the Bank. A positive sentiments from the third tranche of the IMF Extended Credit Facility and agreement in principle with external creditors5, has also ease pressure on the Cedi. But for corporate and consumers the pressure remains strong with the average lending rates of banks standing at 31.10 percent.

Outlook

The international economic situation remains unstable because of continued uncertainties in the Russia-Ukraine war and conflicts in the Middle-East. However, the main fiscal indicators have improved between 2023 and the first half of 2024, despite the continued volatility of the Cedi. On June 24 2024 the government announced that the country and representatives of bondholders had reached agreement in principle on the terms of the Eurobonds restructuring6. This is an important step in the country's long road to economic recovery and debt sustainability.

Related Articles

BIBLIOGRAPHY

1❩ https://www.bog.gov.gh/wp-content/uploads/2023/02/FAQs-Regulatory-sandbox_New-Communications.pdf

2❩ https://mofep.gov.gh/sites/default/files/news/Suspension-of-Payments-on-Selected-External-Debts-of-The-GoG.pdf

3❩ Special press briefing by the Governor of the BoG 21st August 2023.

4❩ Bank of Ghana (2024): Monetary Policy Committee Press Release July, 2024 https://www.bog.gov.gh/wp-content/uploads/2024/07/MPC-Press-Release-July-2024-1.pdf

5❩ The relationship between interest rates on investments and the length of time the investment must be held is called the yield curve. Rates are derived from the market, assuming that at any time, there will be a set of coupon and/or zero-coupon bonds with different terms-to-maturity and cash-flow streams, enough liquidity and no default.

6❩ https://www.mofep.gov.gh/news-and-events/2024-06-24/the-government-of-the-republic-of-ghana-and-representatives-of-bondholders-reach-an-agreement-in-principle-on-the-terms-of-the-eurobonds-restructuring