The art and science of asset allocation in Ghana

Anderson Ansah, Accra, Ghana

February 17, 2024

F und managers and banks handle the financial assets of individuals and also public and private institutions. They perform this function by investing in securities that are available and within the boundaries of existing legislations. They have to comply with the mandate granted to them by investors. Fund managers and banks use different assets classes to construct their investment portfolios. Asset allocation is the process of distributing or allocating investments across multiple asset classes, such as equity, fixed income, debt, cash, and alternatives.

The goal is to reduce risk and potentially increase your returns. Factors influencing asset allocation are investor expectations, risk tolerance, horizon, regulations and the economic environment. Other parameters the fund manager will consider, especially in an international setting, include geographical opportunities, currency exposure and interest rates, which depends on government economic policies.

Overview

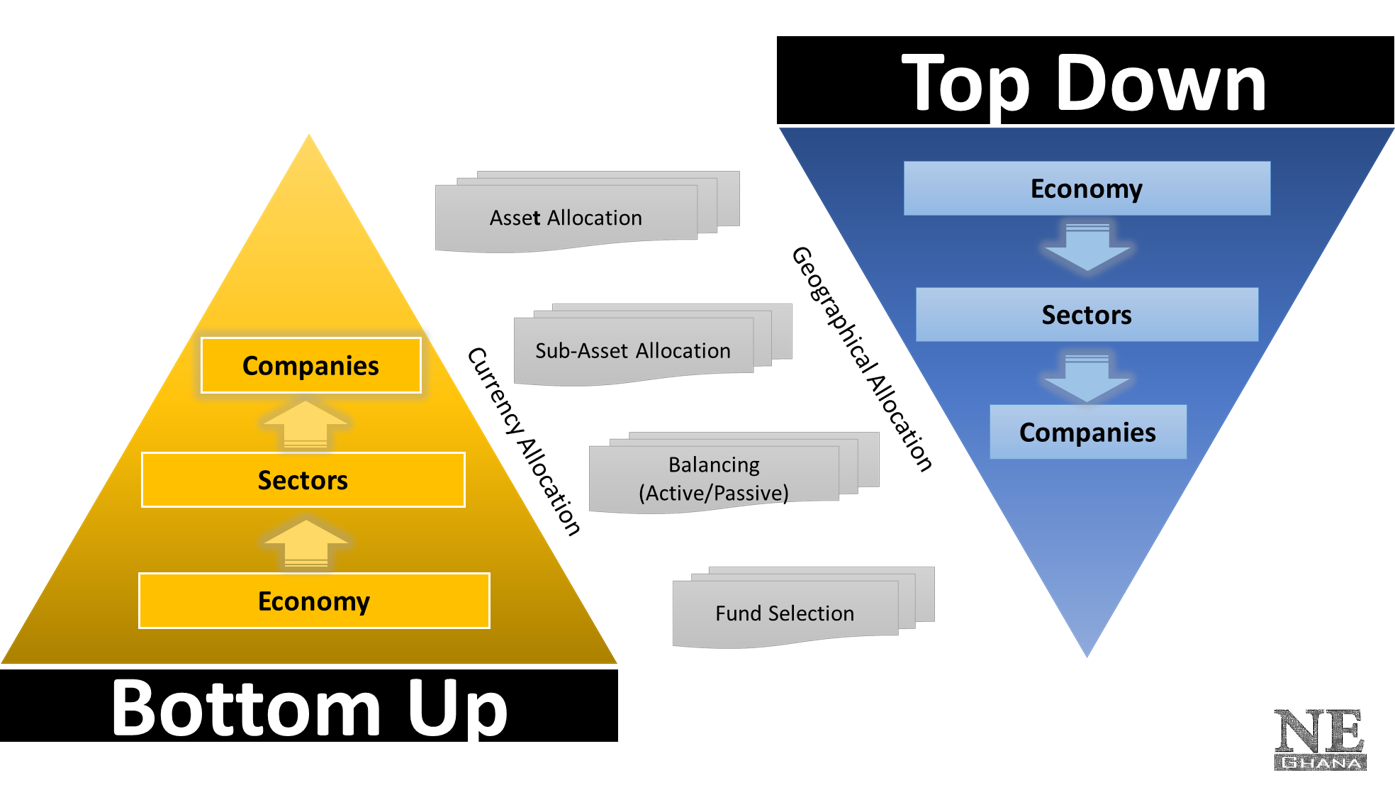

A conventional asset allocation policy specifies one of the two following approaches. The first is the top-down analysis, which begins with a consideration of macroeconomic conditions. Here, analysts evaluate markets and industries to select the assets that have a high probability of performing well under given economic scenarios. The bottom up approach, on the other hand, emphasises economic cycles or industry analysis. This second approach focuses on company-specific circumstances, looking at the quality and experience of the management and the business prospects.

The process requires a careful spread of risks in the portfolio and follows key guiding principles. At the onset, investors expect the portfolio risks to be commensurate with expected return. Second, investors want at least a risk-free rate as return from their portfolio1. The risk-free rate also serves as a benchmark for the return on risky assets. Finally diversification is not only a way of optimizing return, it is also a risk management strategy2.

Conventional asset allocation approaches

Ghana has laws that regulate asset allocation especially for licensed investment schemes. We focus on pension funds, banks, collective investments, and insurance companies.

Pension funds

The goal of asset allocation of pension funds is to meet the future needs of retiring workers. In Ghana, the National Pensions Regulatory Authority (NRPA) has guidelines for pension funds.

• The holding of pension in a single asset of foreign securities must not exceed five percent of its portfolio. Investments in a particular class of shares and debt must not exceed 10 percent of the total funds.

• Pension fund may invest in bonds and other securities issued by the Government of Ghana. In the money market, the cap increases to 35 percent of assets. Examples of instruments include certificates of deposit and banker acceptance.

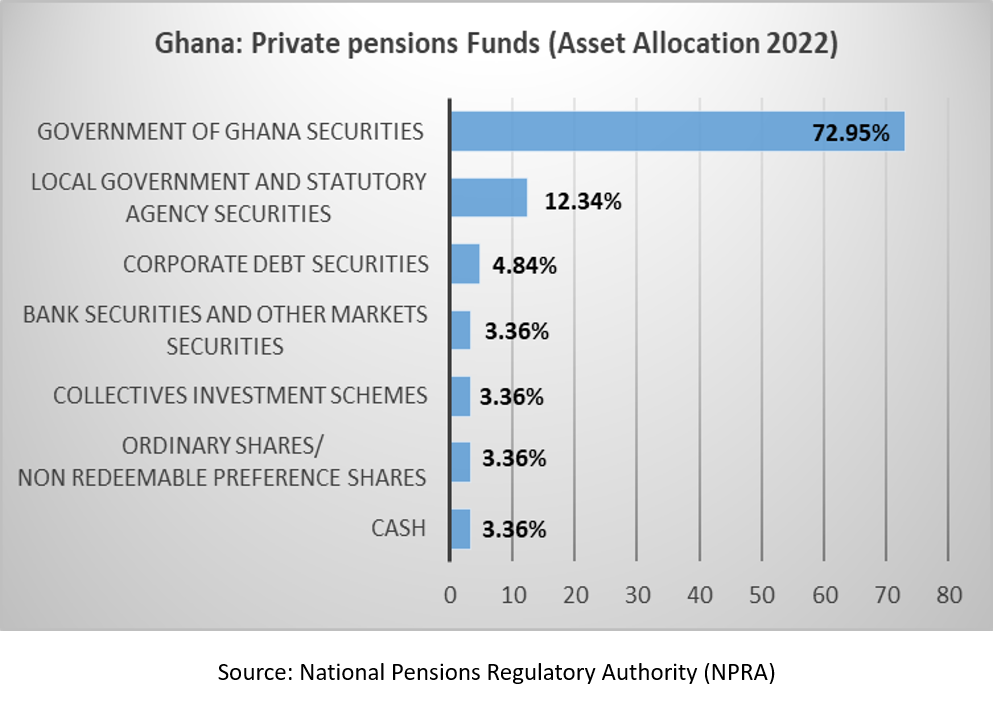

Private pension funds (2022)

• The NRPA3 prescribes a maximum of 30 percent investment in local government securities. But the NRPA also imposes a cap of 5 percent for a single local government.

• For corporate bonds, the regulator allows a maximum of 30 percent investment. But there is also a cap of 5 percent in single bonds, REITs4, MBS5 (Mortgage-backed securities) and debentures.

• The NRPA allows only a maximum of 10 percent investment in ordinary shares of companies quoted on the Ghana Stock Exchange.

• Investment in ordinary shares of a single corporate entity must not exceed 5 percent and no more than 2 percent of the value of pension fund Assets, managed by an approved trustee or pension fund manager, shall be invested in close-end, open-end and hybrid investment funds.

At the first quarter of 2024, pension funds had US$3.24 billion (GH₵ 49.59 billion) under management, with 84 percent of funds invested in government of Ghana securities.

Banks

Banks have more leeway in capital allocation. For banks, the goal of capital allocation is the short-term maximization of shareholder's return. In addition, regulators expect an alignment between asset and liability management and compliance with regulatory capital. Banks follow diverse capital allocation strategies and also see capital allocation as an integral part of risk management.

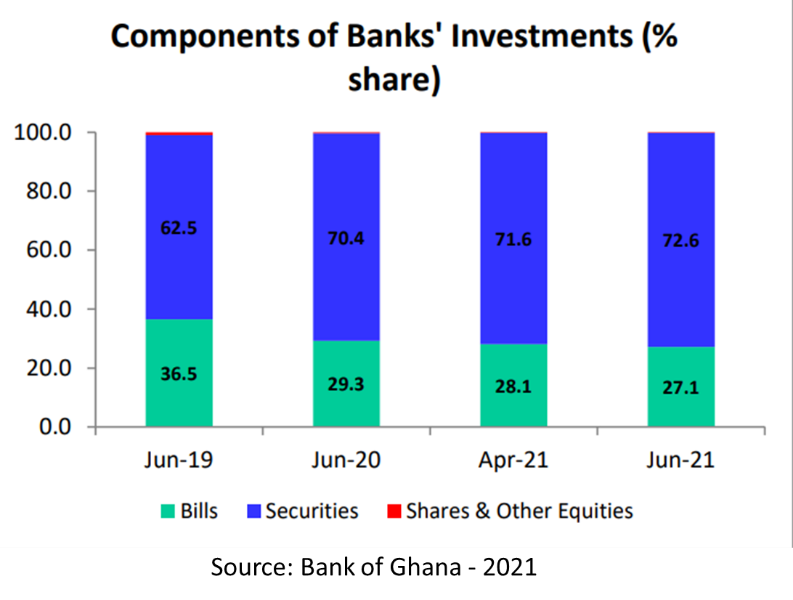

In June 2021, data from the Bank of Ghana showed that the investment portfolio of banks contained substantial long-term debt instruments.

Bank Asset Allocation

The share of securities increased to 72.6 percent in June 2021 (from 70.4 percent in June 2020). Short-term bills in total investments declined to 27.1 percent (from 29.3 percent) during the same comparative periods. Equity investments, however, remained small at 0.3 percent (from 0.4 percent in 2020)6.

Collective investment scheme

The Ghana Security and Exchange Commission (SEC) defines collective investment schemes as pool funds, managed on behalf of investors by a professional fund manager. The 2016 Securities Industry Act (Act 929) provides other characteristics of pooled funds. Holders of interests in the unit trust must approve changes in the asset allocation through a special resolution. These funds invest in short-term securities of less than one year to maturity. Mutual funds and unit trusts specialize in fixed income, equity, money markets, or real estate.

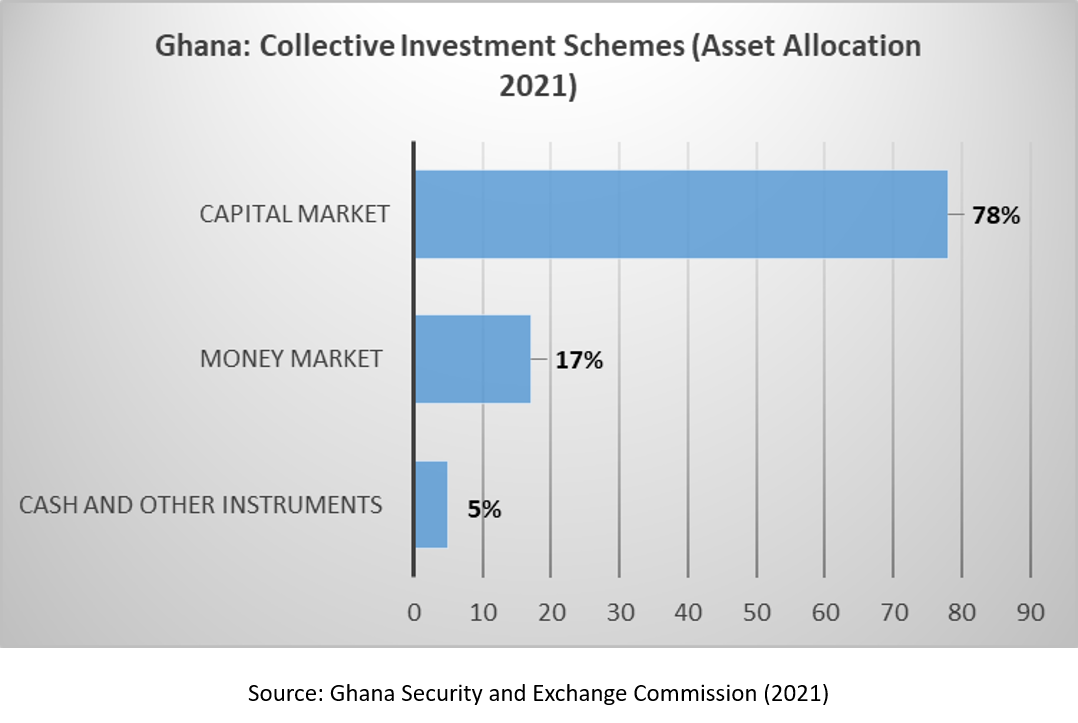

Collective Investments Asset Allocation

This segment of Ghana’s financial markets is growing. During the first quarter of 2023, the Ghana SEC supervised and regulated 49 mutual funds and 34 unit trusts, with US$1.1 billion (GHC 14.9 billion) under management.

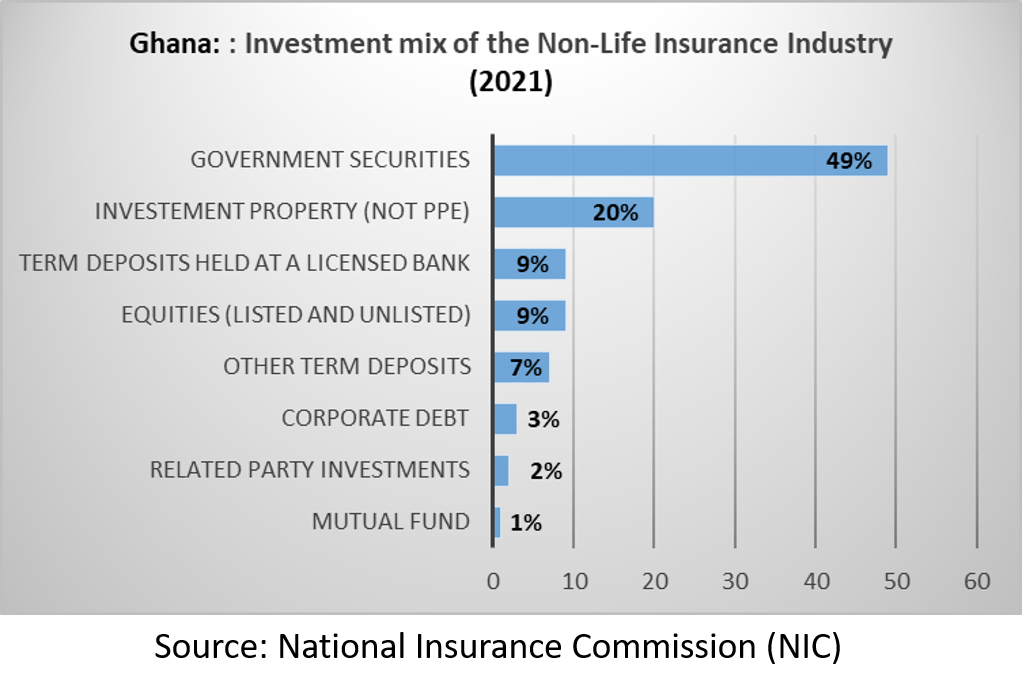

Insurance

The National Insurance Commission (NIC) regulates the insurance sector. In 2021, Ghana had 28 non-life, 20 life, and three re-insurance companies. This industry has US$802 million (GH₵9.2 billion) under management. In 2021, the investment portfolio of non-life insurance companies contained government of Ghana securities (33 percent), bank term deposits (21.6 percent), equities (20.3 percent) and investment property (17.8 percent )7.

Insurance Asset Allocation

Non-life and life insurers prefer holdings in government securities.

Insurance penetration remains low at one percent. A lack of understanding of the benefits of life and non-life insurance coverage continues to stifle the market8. However, bancassurance offers opportunities for growth in the coming years. Bancassurance is an arrangement between a bank and an insurance company, which gives the bank the right to sell insurance products to the bank's customers.

Related Articles

BIBLIOGRAPHY

1❩ Note: These bonds can still be subject to interest rate risk, because real interest rates change unpredictably depending on the business cycle.

2❩ The risk that remains even after extensive diversification is called market risk, risk that is attributable to market wide risk sources. Such risk is also called systematic risk, or non-diversifiable risk.

3❩ https://npra.gov.gh/assets/documents/3RD-EDITION-ISSUE-2-v2.pdf

see also

https://npra.gov.gh/assets/documents/GUIDELINES-ON-INVESTMENT-OF-SCHEME-FUNDS.pdf

3❩ Real Estate Investment Trusts (REITs). REITs invest in real estate or loans secured by real estate. Besides issuing shares, they raise capital by borrowing from banks and issuing bonds or mortgages. Most of them are highly leveraged, with a typical debt ratio of 70 percent.

4❩ MBS are debt obligations that represent claims to the cash flows from pools of mortgage loans, most commonly on residential property. Mortgage loans are purchased from banks, mortgage companies, and other originators and then assembled into pools by a governmental, quasi-governmental, or private entity.

5❩ https://www.bog.gov.gh/wp-content/uploads/2021/08/Banking-Sector-Developments-July-2021-1.pdf

6❩ https://www.bog.gov.gh/wp-content/uploads/2021/08/Banking-Sector-Developments-July-2021-1.pdf

7❩ https://nicgh.org/wp-content/uploads/2023/06/2021-NIC-Annual-Report.pdf

8❩ https://www.gcbbank.com.gh/research-reports/sector-industry-reports/397-insurance-industry-in-ghana-august-2023-1/file